Canadian housing market highly vulnerable, reports mortgage insurer

The Canadian housing market is “highly vulnerable,” which could lead to price corrections. Should Canadians be concerned?

Housing markets in certain Canadian cities have seen a rise in prices that cannot be explained solely by income, interest rates and population growth, according to a report by the Canadian Mortgage and Housing Corp. (CMHC).

The quarterly Housing Market Assessment, based on data from April 2017 to June 2017, suggests that the national housing market is at a “high degree of vulnerability” due to overvaluation and acceleration.

[Photo © Micaal Ahmed]

The CMHC determines overvaluation by comparing actual housing prices to predicted prices based on a CMHC formula that considers income, interest rates and population growth. A market is considered to have moderate or high overvaluation if it experiences price increases not based on typical economic indicators.

When the market is balanced, house prices are expected to increase in line with the cost of living. Acceleration occurs when there is a sustained rise in house prices that is not based on an increased cost of living and could be due to speculation.

The national assessment is highly skewed by Toronto and Vancouver, the two largest markets, where prices have been steadily increasing.

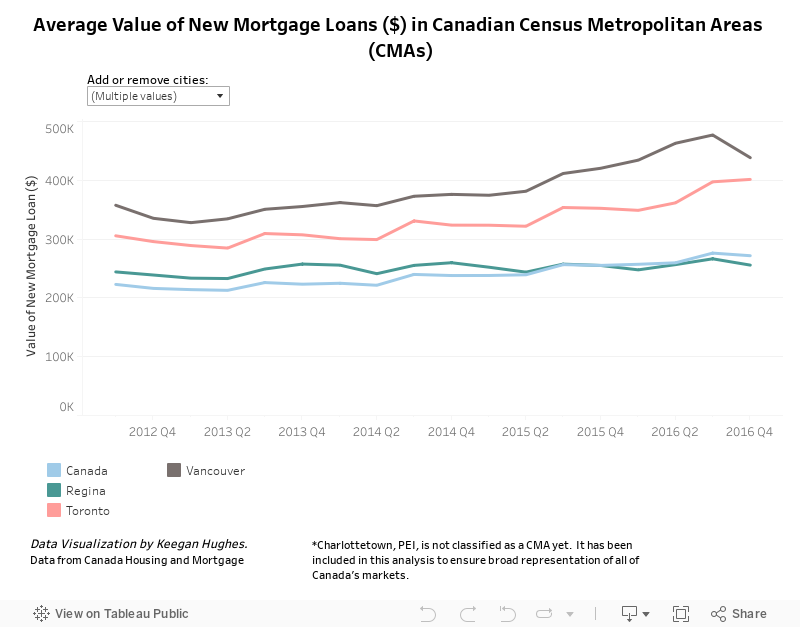

The most recently available data from the CMHC shows that between the fourth quarter of 2012 and 2016 the average new mortgage loan in Toronto rose from $295,934 to $401,728, representing an increase of 36 per cent. The data does not distinguish between dwelling types, such as condominiums or single-detached homes.

“A lot of national vulnerability is really driven by Vancouver, Victoria, Hamilton, and Toronto,” said Tsur Somerville, associate professor at the University of British Columbia’s Centre for Urban Economics and Real Estate. Toronto and Vancouver are the two markets with “the biggest concern about prices being very disconnected from underlying fundamentals.”

In addition to overvaluation and acceleration, the report also identifies overheating and overbuilding as impacting the stability of house prices in certain regions.

“There are growing concerns of overbuilding in Calgary, Edmonton and St. John’s specifically due to higher levels of new and unsold homes compared to the demand for these units,” said CMHC’s Housing Market Assessment report.

Can government intervention stabilize housing markets?

Recent changes to mortgage requirements indicate that policymakers may be concerned by the level of vulnerability in the housing market, but there is no uniform response to a problem with many variables.

“Things that you might do to help out the prairies are not the same things you would do for Vancouver and Toronto when what you are really worried about is high values,” said Somerville.

For example, in 2014, the CMHC decided to no longer provide mortgage insurance for homes that costs $1 million or more, meaning that these borrowers must provide a down payment of at least 20 per cent. This measure impacts specific markets while leaving the others relatively untouched.

[Photo © Micaal Ahmed]

Mortgages over $1 million “are an issue in Toronto and Vancouver,” said Somerville. “But not a lot of people in Regina don’t really worry about that.”

Provincial measures can complement federal mortgage regulations. British Columbia and Ontario have implemented foreign buyer’s taxes on residential properties. However, according to economist Livio Di Matteo, “the long-term impact in cooling off housing markets is not yet evident.”

In Feb. 2016, six months before British Columbia implemented an additional 15 per cent property transfer tax on foreign buyers, the Real Estate Board of Greater Vancouver reported an average price for single-detached homes of $1,816,487. In Aug. 2016, the month the foreign buyers tax was implemented, the average price of a single-detached home dropped by 16 per cent to $1,532,242 before rebounding to $1,758,813 in Feb. 2017, a drop of only 3 per cent from the year before.

High prices, low mortgage defaults

The rising home prices in some markets should be cause for some concern for the CMHC, according to Somerville.

“As a mortgage insurer, they are worried about things that would cause defaults,” he said. “If house values fall below the outstanding mortgage, you would be more likely to see mortgage defaults and they are particularly worried about that because that’s part of their business.”

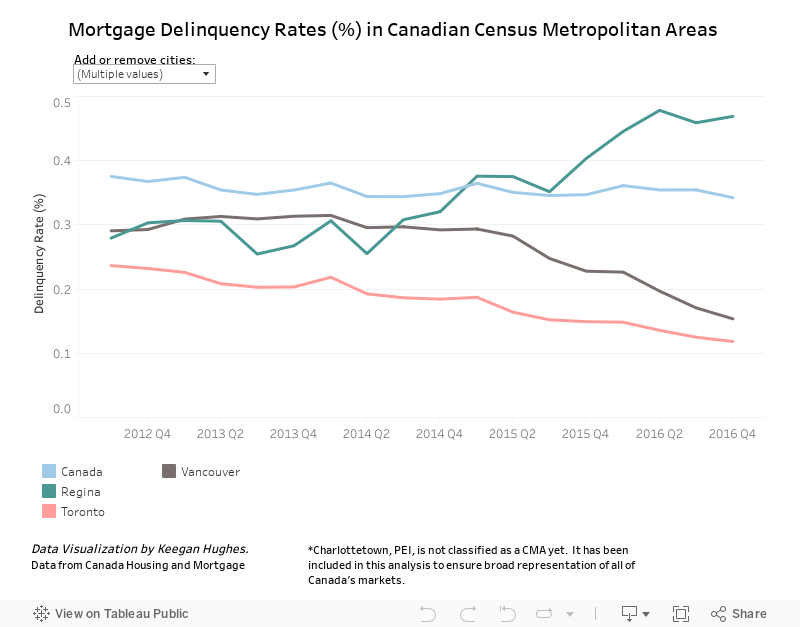

But despite soaring housing prices, there is little evidence of mortgage defaults. The most recently available data from the CMHC indicates a national mortgage delinquency rate of 0.34 per cent in the fourth quarter of 2016. In Toronto and Vancouver, the rates are 0.12 per cent and 0.15 per cent, respectively, or less than half the national rate. According to Tom Storey, a Royal LePage agent in the Toronto area, a hot housing market can save those struggling to make mortgage payments.

“In Toronto, household values have gone up so much that even if someone had a mortgage issue they could just sell their house,” said Storey. Foreclosures and defaults “may be happening but we’re not hearing about it and we’re definitely not seeing it.”

Household affordability

Another factor to consider in a highly vulnerable housing market is affordability. The CMHC considers housing affordable if shelter costs (mortgage, rent, electricity, heat, water, other municipal services, property taxes, and condominium fees) are less that 30 per cent of before-tax household income. This means that a household earning the national median of $70,336 must not exceed $1,758 per month in shelter costs or it would be considered unaffordable.

The 2016 Census results released in October by Statistics Canada show that 24.4 per cent of the population is living in situations that are considered unaffordable. Again, there are striking regional differences with Toronto and Vancouver having the highest proportion of unaffordability, 33.4 per cent and 32 per cent respectively.

While mortgage delinquency rates are low, Statistics Canada says that the household debt-to-income ratio is high – a situation that parallels the U.S before the housing bubble crisis. But according to economist Di Matteo, Canadians shouldn’t be overly worried about a similar crash.

“The problem is not debt, but poorly managed debt,” said Di Matteo. “To date, Canadians have been able to manage their debt load because interest rates are low and the economy has not gone into recession.”

Low interest rates and a stable economy are good news for homeowners if the current conditions persist, but a “high degree of vulnerability” introduces uncertainty to the future stability of housing markets and that makes predictions challenging.

Cyclists like city’s first advisory bike lanes, Ottawa says

Ottawa's first advisory cycling lane rolled out last October provides the city...